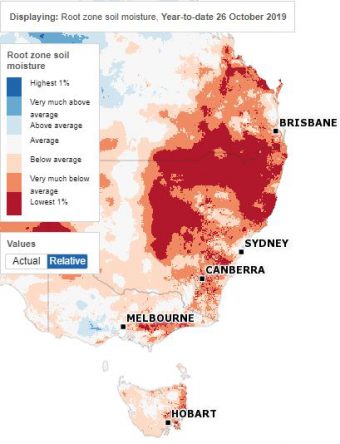

Concerns are mounting over this season’s sorghum production

Concerns are mounting over this season’s sorghum production… It is now the end of October, two months into the summer…

Concerns are mounting over this season’s sorghum production… It is now the end of October, two months into the summer…

International wheat prices continued to firm last week on the back of crop downgrades in the southern hemisphere, delays to…

Many European regions recorded record high temperatures last week as the continent sweltered through its second heatwave of the summer.…

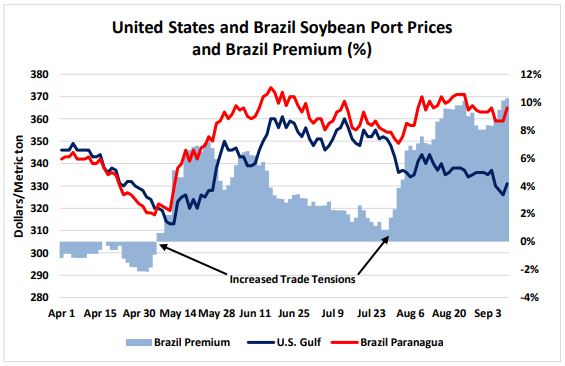

World agricultural commodity markets look set for continued volatility as the trade truce between the United States (US), and China…

The annual Pro Farmer Crop Tour was conducted across seven of the most important corn and soybean states in the…

News that a Chinese trade delegation had cancelled this week’s planned visit to farms in the states of Montana and…

The global grain markets were rocked last week when the United States Department of Agriculture (USDA) amended this season’s US…

Kazakhstan, one of the most important grain producers and exporters in the world, announced last week that it was aiming…

World grain markets trod water early last week ahead of Thursday’s release of the October World Agricultural Supply and Demand…