Australia losing relevance as a global wheat exporter…

The Australian Bureau of Statistics released their July export data last week and the grain numbers undoubtedly reflect the effects…

The Australian Bureau of Statistics released their July export data last week and the grain numbers undoubtedly reflect the effects…

Last year’s Australian winter crop production was the lowest in more than a decade after drought in the eastern states…

The first official Canadian crop estimates for the 2019/20 crop year were released last Wednesday by Statistics Canada, the national…

Egypt’s demand for wheat and corn is growing… Population growth and increased feed grain requirements are expected to drive up…

Grain Brokers Australia Weekly Market Report by Peter McMeekin – 16th October, 2018 During the second week of each month…

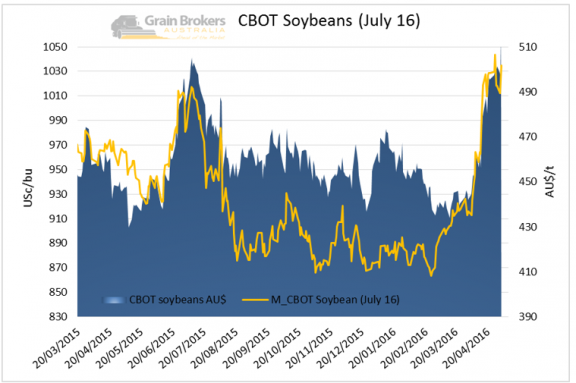

BEANS/CANOLA July-16 Chicago soybean futures made strong gains as the market was boosted by further confirmation of crop damage in…

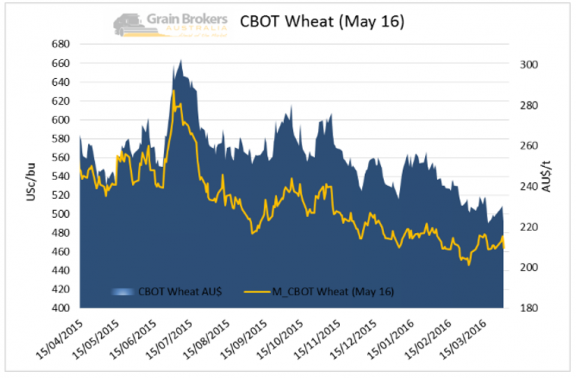

WHEAT Wheat futures rallied last week, as funds extended technical short-covering and reports of firmer export demand helped futures to…

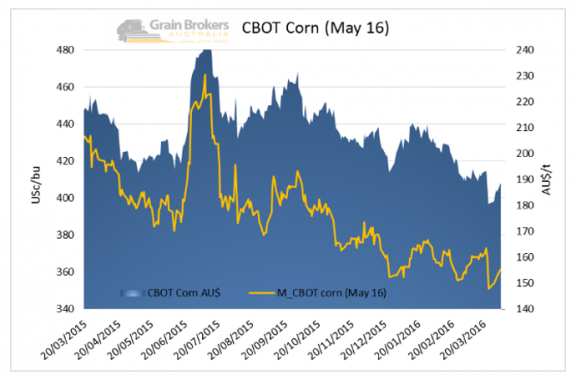

BARLEY/CORN Unlike Wheat, Chicago May-16 corn futures closed up on the week. The increase is thought to be prices recovering…

WHEAT Wheat futures ended the month of March up, as dryness continues to build in the US southern states. CBOT…