US-China trade deal ‘totally done’…

Farmers in the United States have received an early Christmas present after Beijing and Washington finally arrived at a preliminary…

Farmers in the United States have received an early Christmas present after Beijing and Washington finally arrived at a preliminary…

Canadian farmers produced the smallest canola crop in four years on the back of lower plantings and unusually wet autumn…

African Swine Fever (ASF) continues to decimate the domestic pig herd in China with hundreds of millions of animals now…

The news late last week that the Ministry of Commerce (MOFCOM) of the People’s Republic of China had decided to…

International wheat prices continued to firm last week on the back of crop downgrades in the southern hemisphere, delays to…

World agricultural commodity markets look set for continued volatility as the trade truce between the United States (US), and China…

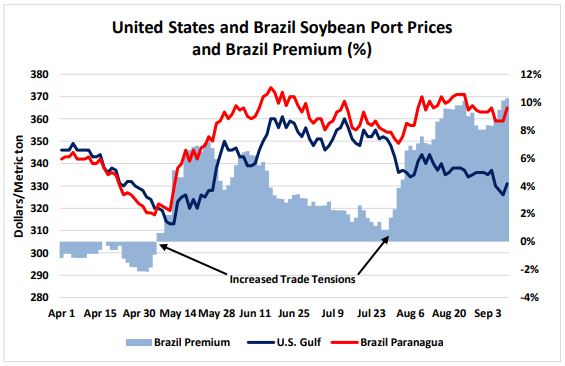

News that a Chinese trade delegation had cancelled this week’s planned visit to farms in the states of Montana and…

Kazakhstan, one of the most important grain producers and exporters in the world, announced last week that it was aiming…

World grain markets trod water early last week ahead of Thursday’s release of the October World Agricultural Supply and Demand…