Indian Ocean Dipole returns to neutral territory…

Extreme weather conditions and unprecedented bushfires across many parts of the Australian continent have been dominating the news cycle over…

Extreme weather conditions and unprecedented bushfires across many parts of the Australian continent have been dominating the news cycle over…

Wheat – With CBOT wheat futures up 18 cents for the week, (or A$7 per tonne) we would have expected…

Last week we had the latest USDA report into US planted acres and grain stocks. While we expected some increases…

It is great to see such a positive start to the season for most across WA with solid early rains…

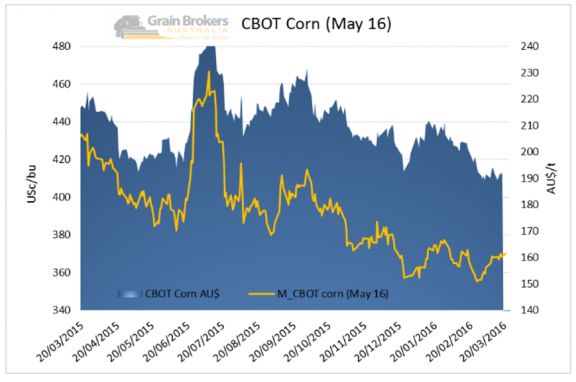

CORN/BARLEY Corn prices have traded above the crucial support of US$3.60. March 16 CBOT corn futures settled the week at…

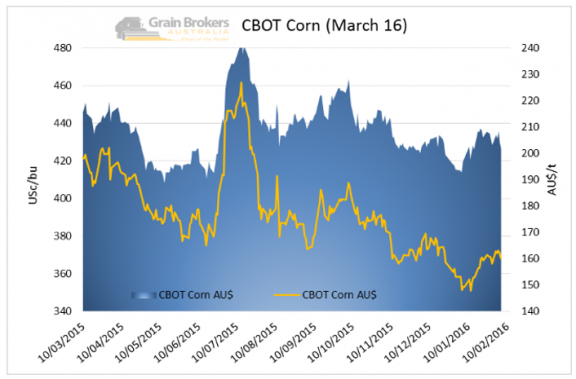

CORN/BARLEY March 16 CBOT corn futures closed higher at US$3.68 per bushel up 3.0 Usc/bu for the week. …

WHEAT CBOT Dec 15 futures finished the week at 526.3USc/bu. An 11.30 USc/bu rise week on week. …

WHEAT Wheat CBOT Dec 15 futures made positive gains for the week, and finished at 515USc/bu. up 24.4USc/bu week on…

BEANS/CANOLA Soybean November 15 CBOT futures were down 6.6USc/bu for the week, from 905.2USc/bu to settle at 898.60USc/bu. ICE…