Weekly Strategy Update 09/11/16

Wheat – Recommend growers establish minimum tonnes they need to sell as required for cash flow accompanying sales of other…

Wheat – Recommend growers establish minimum tonnes they need to sell as required for cash flow accompanying sales of other…

Last Friday we saw one of the biggest days in financial markets of all time with the surprise announcement that…

Wheat pricing this season has been frustrating for growers holding onto grain well after harvest in anticipation of better pricing…

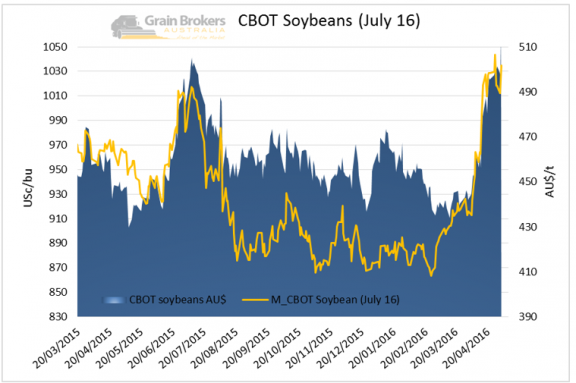

BEANS/CANOLA July-16 Chicago soybean futures made strong gains as the market was boosted by further confirmation of crop damage in…

WHEAT Wheat futures rallied last week, as funds extended technical short-covering and reports of firmer export demand helped futures to…

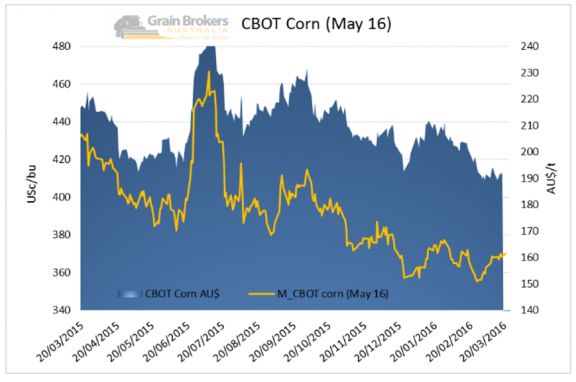

CORN/BARLEY Corn prices have traded above the crucial support of US$3.60. March 16 CBOT corn futures settled the week at…

WHEAT Wheat futures closed lower this week as the market shifted concerns from crop production weather concerns in the short…

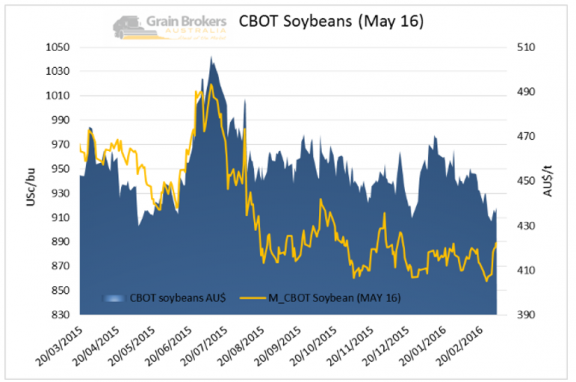

BEANS/CANOLA Chicago May-16 soybean rallied and settled at 889.2 US¢/bu on Friday, the sharp rise owing to strong soybean oil…

With last week’s USDA report not bringing a lot of change to the table other factors are starting to influence…