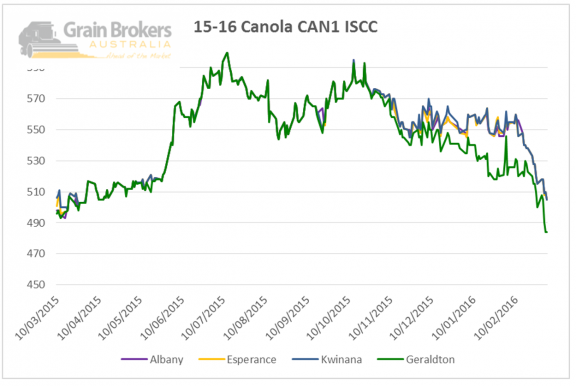

Canadian farmers can’t take a trick this year…

Canadian farmers produced the smallest canola crop in four years on the back of lower plantings and unusually wet autumn…

Canadian farmers produced the smallest canola crop in four years on the back of lower plantings and unusually wet autumn…

Click here for Varietal Grouping Lists 2019/20 Season – Variety Listings – 19-20

The annual Pro Farmer Crop Tour was conducted across seven of the most important corn and soybean states in the…

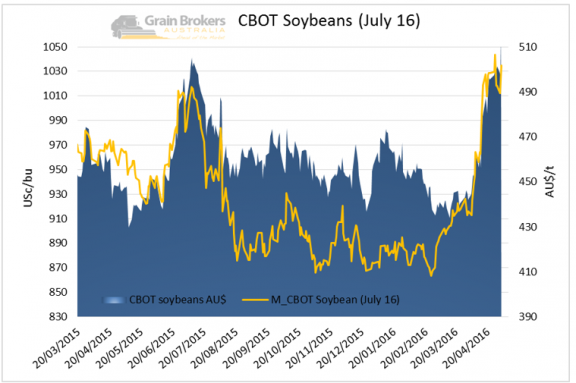

BEANS/CANOLA July-16 Chicago soybean futures made strong gains as the market was boosted by further confirmation of crop damage in…

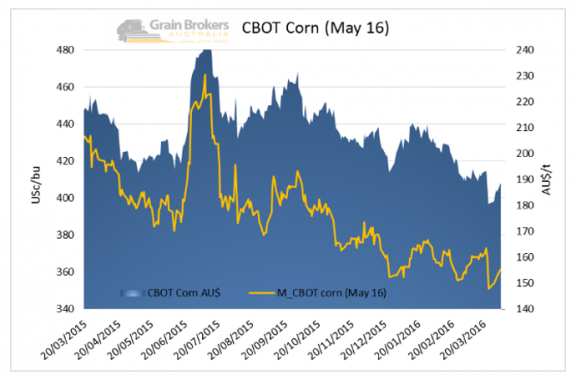

BARLEY/CORN Unlike Wheat, Chicago May-16 corn futures closed up on the week. The increase is thought to be prices recovering…

BEANS/CANOLA Chicago May-16 soybean rallied and settled at 889.2 US¢/bu on Friday, the sharp rise owing to strong soybean oil…

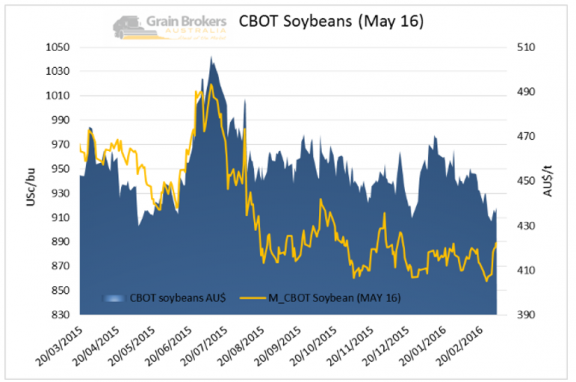

BEANS/CANOLA Chicago May-16 soybean prices increased 1% and settled at 863.6 US¢/bu on Friday, as the sharp rise in Brazilian…

CORN/BARLEY In a subdued finish to 2015 corn hit new contract lows of US$3.57 during the week. March 16 CBOT…

CORN/BARLEY Dec 2015 CBOT corn futures fell by 12.4USc/Bu and settled at US$3.745 per bushel. Global corn demand was forecast…