Barley anti-dumping investigation remains a sleeping giant

The news late last week that the Ministry of Commerce (MOFCOM) of the People’s Republic of China had decided to…

The news late last week that the Ministry of Commerce (MOFCOM) of the People’s Republic of China had decided to…

The United States Department of Agriculture (USDA) released their November World Agricultural Supply and Demand Estimates (WASDE) to the market…

Farmer selling has picked up over the past week as the 2019 harvest gathers momentum in the southern grain-growing regions…

Click here for Varietal Grouping Lists 2019/20 Season – Variety Listings – 19-20

New segregation for pre-harvest application of glyphosate on feed barley Click the link below to download the flyer with important…

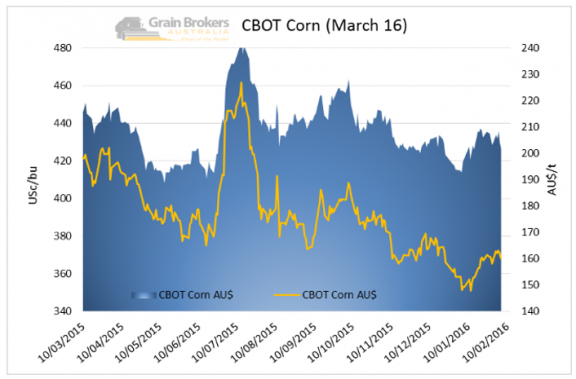

CORN/BARLEY March 16 CBOT corn futures closed higher at US$3.68 per bushel up 3.0 Usc/bu for the week. …

CORN/BARLEY In a subdued finish to 2015 corn hit new contract lows of US$3.57 during the week. March 16 CBOT…

CORN/BARLEY Dec 2015 CBOT corn futures fell by 12.4USc/Bu and settled at US$3.745 per bushel. Global corn demand was forecast…